Social Insurance Scheme (SIS)

Introduction to Korea's social insurance scheme

Definition of social insurance scheme?

Social insurance scheme refers to a socioeconomic program using mechanisms and techniques of insurances in order to fulfill national social policies.

The purpose of the scheme is to realize health & income security for people through providing against their social risks using insurance mechanisms and techniques.

Those social risks, including diseases, disabilities, old age, unemployment, death, etc., cause a great deal of economic difficulties and substantial instabilities to not only people themselves but also their dependents. In this sense, the scheme can be defined as an income security program to economically secure a stable life for people by identifying and providing against social risks to come.

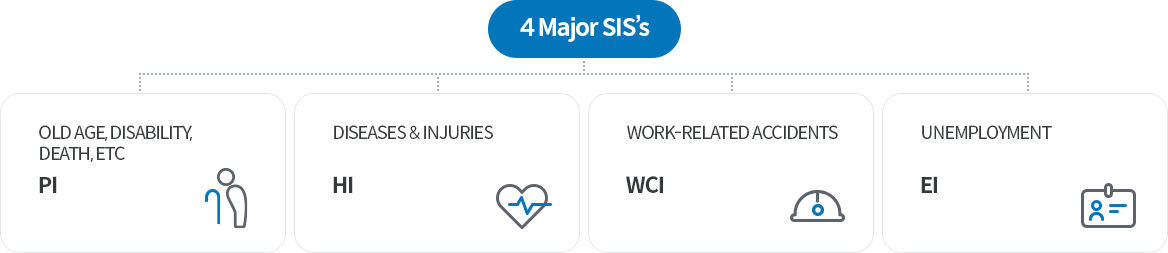

In Korea, there are 4 major social insurance schemes (“SISs”) : workers’ compensation insurance (“WCI”) against work-related accidents; health insurance (“HI”) (or disability insurance (“DI”)) against diseases and injuries; pension insurance (“PI”) against serious disability, death, old age, etc.; and finally, employment (“EI”) against unemployment:

Comparison between social insurance and private insurance

Social solidarity and mandatoriness are characteristics of social insurance. The following shows the comparison between social insurance and private insurance :

| Item | Social insurance | Private insurance |

|---|---|---|

| Purpose | To realize basic livelihood security & medical security | To meet individual-based insurance needs |

| Mandatorily or voluntarily covered | Mandatorily | Voluntarily |

| Shared responsibility for the vulnerable | Governmental or social responsibilities for the vulnerable | Neither governmental nor social responsibilities for the vulnerable |

| Entitlement to due benefits | Legally guaranteed | Contractually guaranteed |

| Monopolistic or competitive | Monopolized by the Government or government organizations | Competitive |

| Who-pays principle | Everybody-pays principle | Mainly, beneficiary-pays principle |

| Premium billing | Pay-as-you-earn | Varying depending on individual insurance needs |

| Premium rating | Mainly, flat rate | Mainly, income-indexed flat rate |

| Premium level | At most premium level corresponding to risk factor | Experience-based |

| Selection of risks to be insured | Not required to select risks to be insured | Required to select risks to be insured |

| Benefit level | Uniformly paid | Contribution-based |

| Inflation-indexation | Inflation-indexed | Mainly, not inflation-indexed |

| Scope of coverage | Bodily injury liability | Bodily injury liability & property damage liability |

| Collectively or individually insured | Collective | Individual |